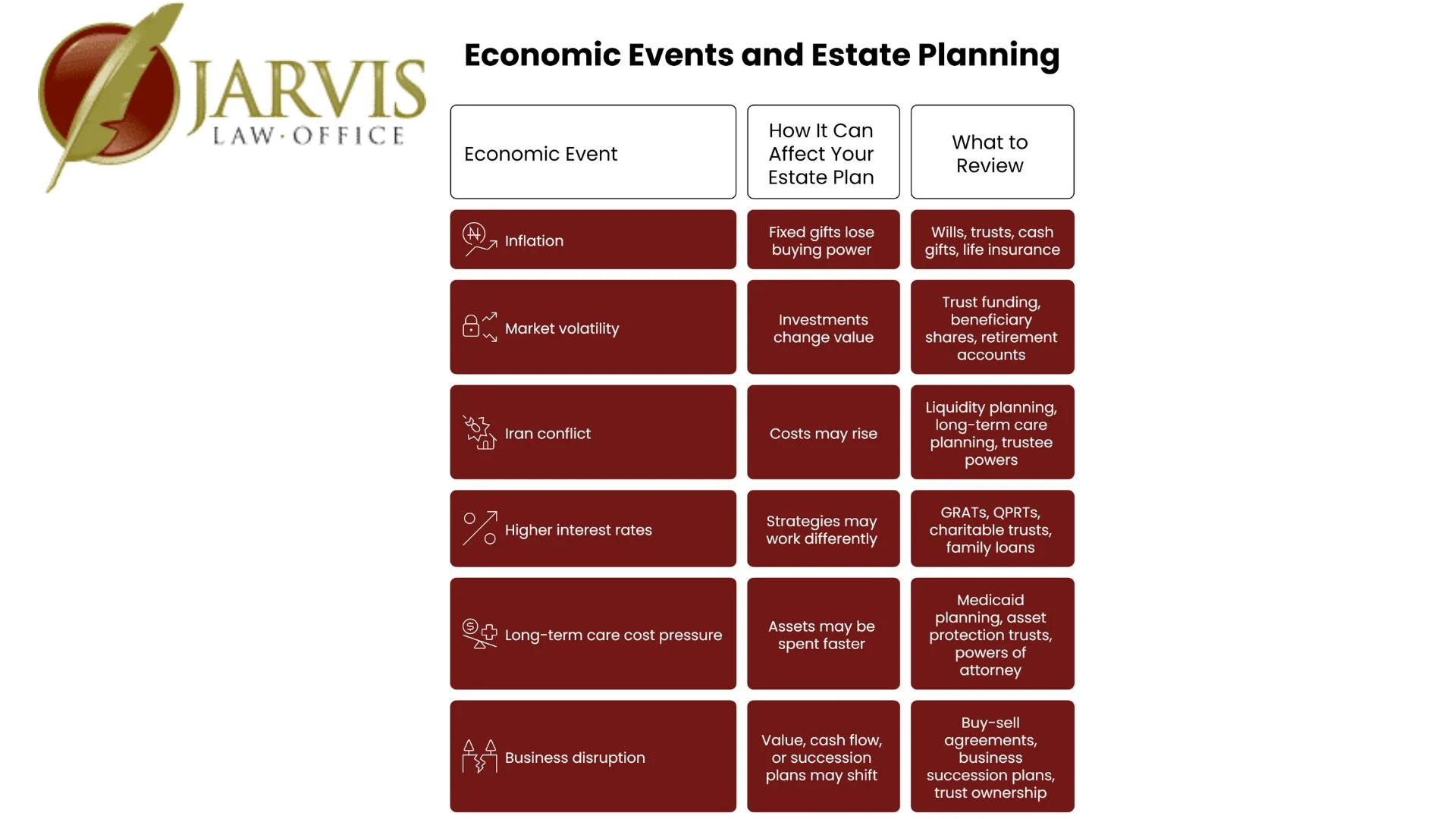

Inflation, market volatility, and global conflict can affect your estate plan by changing asset values and increasing long-term care costs.

According to the U.S. Bureau of Labor Statistics, prices rose 3.3% over the past year, with energy up 12.5% and gasoline up 18.9%.

2026 conflicts show how quickly global events can impact everyday costs. Disruptions in the Strait of Hormuz have raised concerns about oil supply and higher fuel prices, which can ripple into household expenses and investment markets.

For Ohio families, this can mean outdated estate plans. A fixed inheritance may no longer go as far, trusts may hold shifting asset values, and retirement accounts or business plans may need review. Rising care costs can also affect how much is left for beneficiaries.

Jarvis Law Office, P.C. helps Ohio families, retirees, and business owners review these risks with clear estate planning, trust planning, probate avoidance, and asset protection guidance.

How Can Economic Uncertainty Affect Your Estate Plan?

Economic uncertainty affects your estate plan when asset values, care costs, tax rules, or family needs change after your documents are signed.

An estate plan is built around real-world assumptions. It depends on what you own, what your assets are worth, who should receive them, who should make decisions for you, and how much money may be needed for taxes, debts, care, and family support.

Inflation and market swings can change those assumptions faster than many older wills and trusts expect.

Inflation reduces what an inheritance can actually buy over time. A gift that feels meaningful today may cover much less in the future as costs rise.

Fixed Gifts Can Become Outdated

Fixed gifts become outdated when the dollar amount no longer matches your original intent. A $10,000 gift for education, a $50,000 gift for housing, or a cash gift to a charity may not provide the same help later.

This does not mean every fixed gift is wrong. Fixed gifts can work well when the purpose is clear and the amount is reviewed regularly. The risk comes from letting the number sit unchanged while prices, assets, and family needs move.

Life Insurance May Need a Second Look

Life insurance often supports a surviving spouse, pays debts, replaces income, or creates cash for taxes and final expenses. Inflation can make old coverage amounts too low.

A policy bought years ago may not match today’s mortgage balance, care costs, funeral expenses, or family support needs. This is especially important when a surviving spouse depends on the policy to stay in the home or pay for care.

Trusts Should Match Real Family Needs

Trusts should give clear instructions for how money may be used when costs change. Many trusts include standards for health, education, maintenance, and support. Those words matter when a trustee must decide whether to pay for housing, medical care, memory care, transportation, or other needs.

A trustee may also need flexibility. If a trust forces quick distributions or asset sales, the family may lose options during inflation or market stress. Clear trust language helps the trustee follow your wishes without guessing.

Inflation Can Affect Long-Term Care Planning

Market volatility can affect your plan by:

- Changing the value of retirement and investment accounts

- Creating uneven distributions between beneficiaries

- Requiring updated business valuations

- Forcing or delaying asset sales by a trustee

- Reducing income available for a surviving spouse

- Causing beneficiary designations to fall out of sync

These changes affect whether your estate plan still reflects your original intent.

Unequal Asset Values Can Create Unequal Inheritances

When different assets are left to different people, market changes can create uneven results. For example, one child may receive investments while another receives real estate. If values shift, the distribution may no longer match your intent.

A better approach is to review the full estate together, including property, accounts, insurance, and business interests.

Trustees Need Flexibility During Market Swings

Trustees need flexibility to avoid selling assets at the wrong time. Forced sales during a downturn can reduce what beneficiaries receive.

Strong trust language should allow a trustee to:

- Delay sales when needed

- Manage investments during volatility

- Maintain cash for expenses

- Treat beneficiaries fairly

- Work with advisors

A trust should be built to handle changing conditions, not just steady markets.

Retirement Accounts Need Special Review

Retirement accounts often pass by beneficiary designation, not by the will. If those forms are outdated, they can override your estate plan.

This becomes more important when account values grow or shift.

Review:

- Primary and backup beneficiaries

- Whether a trust is named correctly

- Fit for spouses, minors, or special needs beneficiaries

- Tax considerations

Business Owners May Need Updated Succession Planning

Business value can change with inflation, costs, and market pressure. An outdated plan may no longer work.

Review:

- Buy-sell agreements

- Operating agreements

- Trust ownership

- Successor management

- Key-person planning

- Life insurance

- Business valuation

- Family roles

A clear succession plan helps protect both the business and the family.

How Can the 2026 Iran Conflict Affect Estate Planning Decisions?

The 2026 Iran conflict can affect estate planning decisions by increasing energy costs, inflation pressure, investment volatility, and uncertainty around retirement, business ownership, and long-term care planning.

As of April 28, 2026, the conflict has created direct concern around the Strait of Hormuz. The Federal Reserve Bank of Dallas reported that the strait closed after military conflict with Iran began on February 28, 2026, raising concerns about a geopolitically driven oil supply disruption.

For Ohio families, the estate planning issue is not the politics of the conflict. The issue is how higher fuel costs, unstable markets, and rising household expenses affect the plan your family may depend on later.

Oil and Gas Prices Can Affect Family Cash Needs

Oil and gas prices matter for estate planning because higher energy costs can raise the amount of cash a family needs after illness, incapacity, or death.

The U.S. Energy Information Administration reported that flows through the Strait of Hormuz in 2024 and the first quarter of 2025 made up more than one-quarter of total global seaborne oil trade and about one-fifth of global oil and petroleum product consumption.

That matters for an estate plan because fuel and energy costs affect more than the price at the pump. They can affect transportation, food, utilities, care services, and business costs. A surviving spouse, trustee, or agent under a power of attorney may need easier access to cash if everyday expenses rise.

Review these items:

- Cash reserves for a surviving spouse.

- Trust language for emergency distributions.

- Life insurance amounts.

- Powers of attorney.

- Long-term care planning.

- Business succession plans.

Inflation Pressure Can Reduce the Value of Fixed Gifts

Inflation reduces the real value of fixed gifts. A $25,000 inheritance stays the same on paper, but it may cover much less over time.

That is why fixed gifts should be reviewed. Ask:

- Do these amounts still match your intent?

- Would percentages work better?

- Does the trust allow flexibility?

- Has life insurance kept up with costs?

- Are care expenses accounted for?

Jarvis Law Office, P.C. helps Ohio families revisit these details so older plans still reflect current needs.

Market Stress Can Affect Trust Assets and Retirement Accounts

Market changes can shift asset values before they are passed on. If one beneficiary receives investments and another receives real estate, results may become uneven.

Events like the Iran conflict show how quickly markets can move. A trust should give the trustee flexibility to manage assets, delay sales, and maintain cash when needed.

Long-Term Care Planning May Need Earlier Review

Rising costs make long-term care planning more urgent. Care expenses are tied to the same factors driving inflation, including fuel, staffing, and medical costs.

For Ohio families, this often means updating more than a will. Powers of attorney, Medicaid planning, trust funding, and care planning should work together.

Timing matters. Planning early gives families more options and less stress if care is needed.

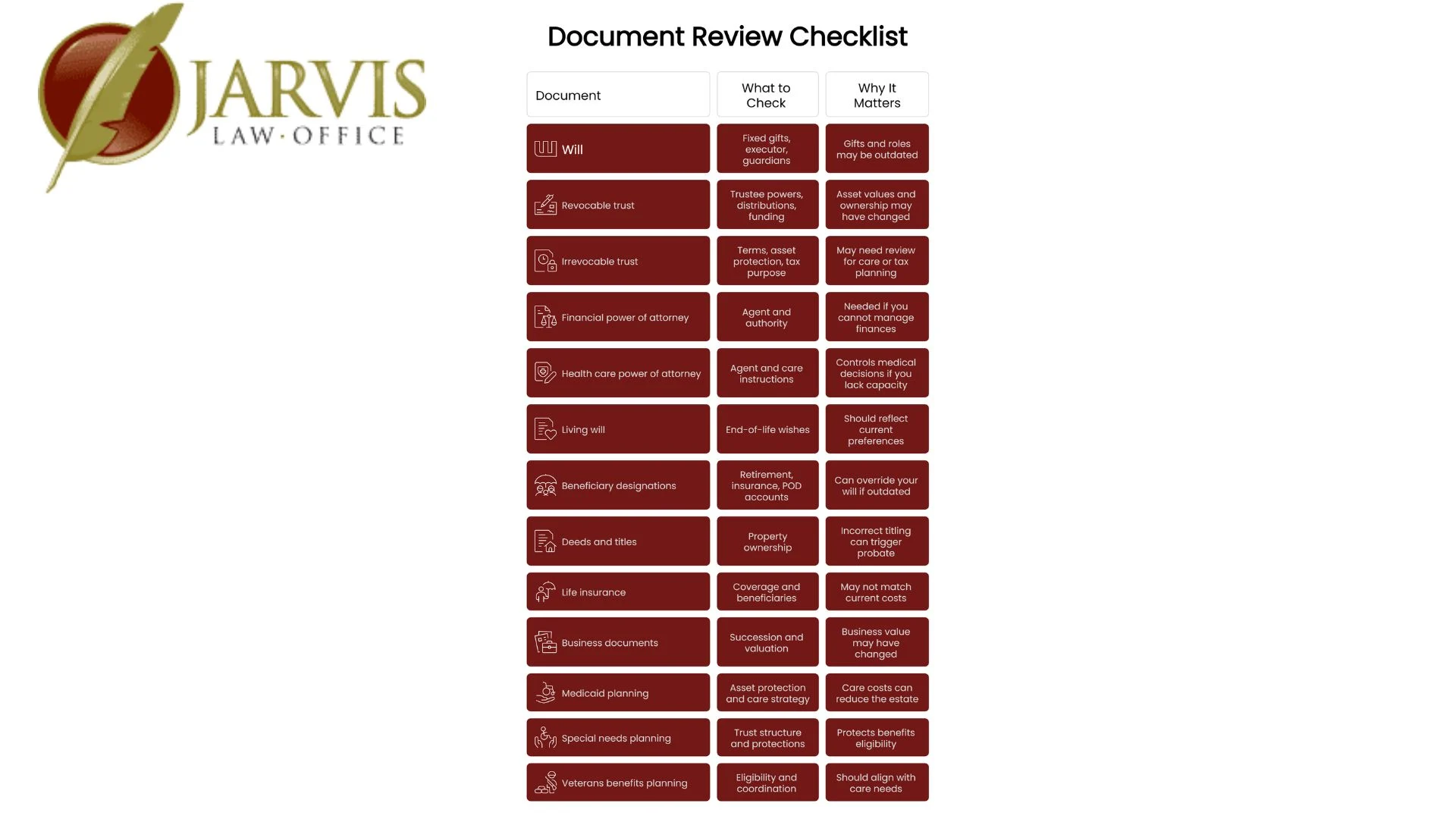

Which Estate Planning Documents Should You Review During Inflation, Market Volatility, or Global Conflict?

You should review the key documents that control asset transfer, decision-making, and long-term care planning. Economic changes do not always require a full rewrite, but they often mean your plan needs updates to match current values and needs.

Review the Will for Fixed Gifts and Family Roles

Your will should reflect your current family and finances. Fixed gifts, executors, and beneficiaries can become outdated over time.

Check:

- Do fixed gifts still match your intent?

- Is the executor still the right choice?

- Are beneficiaries and guardians current?

Review the Trust for Flexibility and Funding

A trust should be reviewed for what it says and what it owns. Both matter.

- Does the trustee have flexibility during market changes?

- Are assets actually titled in the trust?

An unfunded trust may not avoid probate. Jarvis Law Office, P.C. helps make sure assets are properly connected to the trust.

Review Powers of Attorney Before a Crisis

A financial power of attorney allows someone to act if you cannot.

Check:

- Is the agent still the right person?

- Is backup coverage in place?

- Does it allow full financial and legal authority?

Updating this early avoids problems later.

Review Health Care Documents for Current Wishes

Health care documents should reflect your current choices.

Review:

- Health care power of attorney

- Living will

- HIPAA authorization

- Care preferences

Clear documents help your family make decisions without confusion.

Review Beneficiary Designations and Account Titles

Some assets pass by beneficiary form, not by your will.

Check after major life or financial changes:

- Marriage or divorce

- Death in the family

- New accounts or large value changes

- Creation of a trust

Outdated forms can override your plan.

Review Long-Term Care and Medicaid Planning

A will alone does not cover care costs.

Review:

- Medicaid planning options

- Asset protection strategies

- Powers of attorney

- Trust structure

Planning early gives more options and reduces stress.

Why Does Trust Funding Matter More When Asset Values Change?

Trust funding matters more when asset values change because a trust only works for assets that are properly connected to it. A signed trust does not automatically control every home, bank account, investment account, business interest, or insurance policy you own.

In Ohio, trustee powers apply to trust property. Ohio law gives a trustee authority over the investment, management, and distribution of trust property, and it also allows a trustee to collect trust property, sell property, deposit trust money, borrow money, and manage certain business interests when the trust terms allow it.

A Signed Trust Is Not the Same as a Funded Trust

A signed trust gives instructions. A funded trust connects those instructions to your assets.

If assets like your home or accounts are not properly titled to the trust, the trustee may not have authority over them when needed.

Common assets include:

- Real estate (home, rental, farm)

- Bank and brokerage accounts

- Business interests

- Personal property

- Life insurance coordination

- Transfer-on-death or payable-on-death accounts

Retirement accounts require special handling through beneficiary designations.

Unfunded Assets Can Create Probate Problems

Assets left outside the trust may still go through probate.

For example, if a home was never retitled, it may not follow the trust, even if the document says it should.

Review funding after:

- Buying or selling property

- Opening new accounts

- Changing financial institutions

- Receiving an inheritance

- Starting or selling a business

- Refinancing

- Moving states

Probate avoidance depends on both documents and proper asset ownership.

Market Changes Can Shift What Matters Most

Asset values change over time. One account or property may become more important than expected.

Instead of asking, “Do we have a trust?” ask, “Does the trust cover the assets that matter most now?”

Quick check:

- Home: Is the deed correct?

- Accounts: Owned or aligned with the trust?

- Retirement: Beneficiaries up to date?

- Insurance: Correct beneficiary?

- Business: Matches the estate plan?

How Do Estate Taxes Affect Ohio Families During Inflation and Market Changes?

Estate taxes can matter when asset growth pushes an estate toward federal tax limits. While Ohio no longer has an estate tax, federal rules still apply to larger estates, especially for business owners and those with real estate or significant investments.

The IRS sets the 2026 federal estate tax exemption at $15,000,000, with an annual gift limit of $19,000 per person. Many families fall below this threshold, but rising property values, investment growth, or life insurance can increase estate size over time.

Even without Ohio estate tax, taxes can still affect what beneficiaries receive. Retirement accounts may carry income tax, and capital gains or business transfers may require planning.

The key point is that tax planning should work alongside probate avoidance and trust funding. A plan that reduces taxes but leaves assets uncoordinated can still create problems for your family.

Ohio Estate Tax Is Not the Same as Probate

Estate tax and probate are different. Estate tax is about taxes owed. Probate is about court involvement.

You may owe no Ohio estate tax and still go through probate if assets are not properly titled or have no beneficiary. A funded trust and updated beneficiary forms help avoid this.

Federal Estate Tax Still Matters for Larger Estates

Federal estate tax applies to higher-value estates. While many Ohio families are below the threshold, business owners and those with real estate, investments, or life insurance should still review their exposure.

Rising asset values can push an estate closer to tax limits over time.

Asset Growth Can Change the Tax Picture

Estate value is not fixed. Real estate, investments, and business interests can grow.

Review:

- Property and business values

- Retirement accounts

- Life insurance ownership

- Prior gifts

- Tax exposure

An older plan may not reflect current value or structure.

Tax Planning Should Work With Probate Avoidance

Saving taxes does not help if assets are hard to transfer.

For many families, the bigger risk is poor coordination between:

- Trust funding

- Beneficiary designations

- Asset titles

A strong plan focuses on both tax awareness and smooth transfer.

The right strategy depends on your assets, goals, and timing. Market changes can create both risks and opportunities, so flexibility matters.

Common options include:

- Revocable trusts to keep assets organized and avoid probate

- Irrevocable trusts for asset protection and long-term planning

- Annual gifts to transfer wealth gradually (up to $19,000 per person in 2026)

- GRATs for transferring future growth in higher-value estates

- Charitable trusts for combining giving with income or tax planning

- QPRTs for transferring a home under specific conditions

- Family LLCs and succession plans to manage business or real estate ownership

The key is choosing a strategy that fits your overall plan, not just reacting to market conditions.

How Can Long-Term Care Costs and Medicaid Planning Affect Your Estate Plan?

Long-term care costs can affect your estate plan because care expenses may use assets before your beneficiaries ever receive them. A plan that only says who gets your property after death may not protect your spouse, your home, or your savings if care is needed first.

In Ohio, the 2025 CareScout Cost of Care Survey reported monthly median costs of $6,103 for assisted living, $9,186 for a nursing home semi-private room, and $10,389 for a nursing home private room. Home-based care is also expensive, with non-medical caregiver services listed at $6,483 per month in Ohio.

Long-Term Care Can Change What Your Family Inherits

Long-term care costs can reduce what your family receives. Expenses like assisted living, nursing care, and home care are often paid before assets pass to beneficiaries.

Your plan should answer:

- Who can manage accounts if care is needed?

- What assets support a spouse?

- Is the trust funded?

- Are beneficiary forms current?

- Is there a Medicaid strategy?

A will alone is not enough. Care planning requires a broader review.

Medicaid Planning Should Happen Before a Crisis

Medicaid planning works best before care is needed. Ohio uses a five-year look-back period for asset transfers, which can limit options if planning is delayed.

Review:

- Income and savings

- Real estate and insurance

- Retirement accounts and trusts

- Prior gifts

- Care needs and spousal protection

Early planning helps preserve options and avoid costly mistakes.

Estate Recovery Can Affect the Family Home

Ohio Medicaid may seek repayment after death, including from the home.

This is why estate planning and Medicaid planning should work together. A will alone does not protect assets from estate recovery.

Powers of Attorney Matter During Care Decisions

Powers of attorney allow someone to act when needed.

A financial agent may need to:

- Pay bills

- Manage accounts

- Handle property

- Apply for Medicaid

- Work with care providers

Health care documents guide medical decisions and reduce confusion.

Memory Care Planning Needs Early Action

Conditions like dementia can limit the ability to update documents later.

Review early:

- Powers of attorney

- Living will and HIPAA forms

- Trust terms and trustees

- Care instructions

Early planning gives families more control.

Asset Protection Should Match Care Needs

The right strategy depends on your situation. Some families need probate avoidance, others need Medicaid or asset protection planning.

Jarvis Law Office, P.C. helps Ohio families align estate planning, care planning, and trust funding so the plan works when it matters.

Talk With an Ohio Estate Planning Attorney Before Economic Uncertainty Creates Family Stress

Inflation, market volatility, and global conflict can all expose weak points in an older plan.

Jarvis Law Office, P.C. helps Ohio families, retirees, and business owners review these issues. The firm focuses on estate planning, elder law, probate avoidance, trust planning, Medicaid planning, and asset protection.

If your estate plan was created before recent inflation, market swings, care changes, or the current geopolitical uncertainty, now is a good time to review it.

Contact Jarvis Law Office, P.C. through the firm’s contact page to ask whether your will, trust, powers of attorney, beneficiary forms, and asset protection plan still match your family’s needs.