Protecting your assets while following Medicaid eligibility rules requires careful planning. Many people assume they’ll have to spend down their savings or risk losing control of their estate, but there are smarter ways to secure your future.

Understanding the Federal Poverty Level (FPL) guidelines is a key step in Medicaid planning. According to the Department of Health and Human Services, the Federal Poverty Level is adjusted annually, making it necessary to stay updated to better prepare for Medicaid planning.

At Jarvis Law Office, we help families avoid probate and manage assets strategically, allowing for a smooth transition into trusts without unnecessary costs or complications. Our approach keeps you in control, offering a cost-effective, one-time fee solution instead of ongoing expenses.

Updated for 2026

The 2026 Federal Poverty Levels Are Now Available

The U.S. Department of Health and Human Services updates the Federal Poverty Level every year, so the 2025 figures on this page are no longer the current guidelines. If you are working through Medicaid eligibility, long‑term care, or asset protection today, start from the 2026 numbers.

- One-person household: $15,960 at 100% FPL, or about $22,025 at the 138% Medicaid limit

- Household of four: $33,000 at 100% FPL, or about $45,540 at 138%

- Ohio remains a Medicaid expansion state, covering most adults up to 138% of FPL

- Worth noting: subsidies for 2026 ACA Marketplace coverage generally still rely on the 2025 guidelines below

Key Takeaways

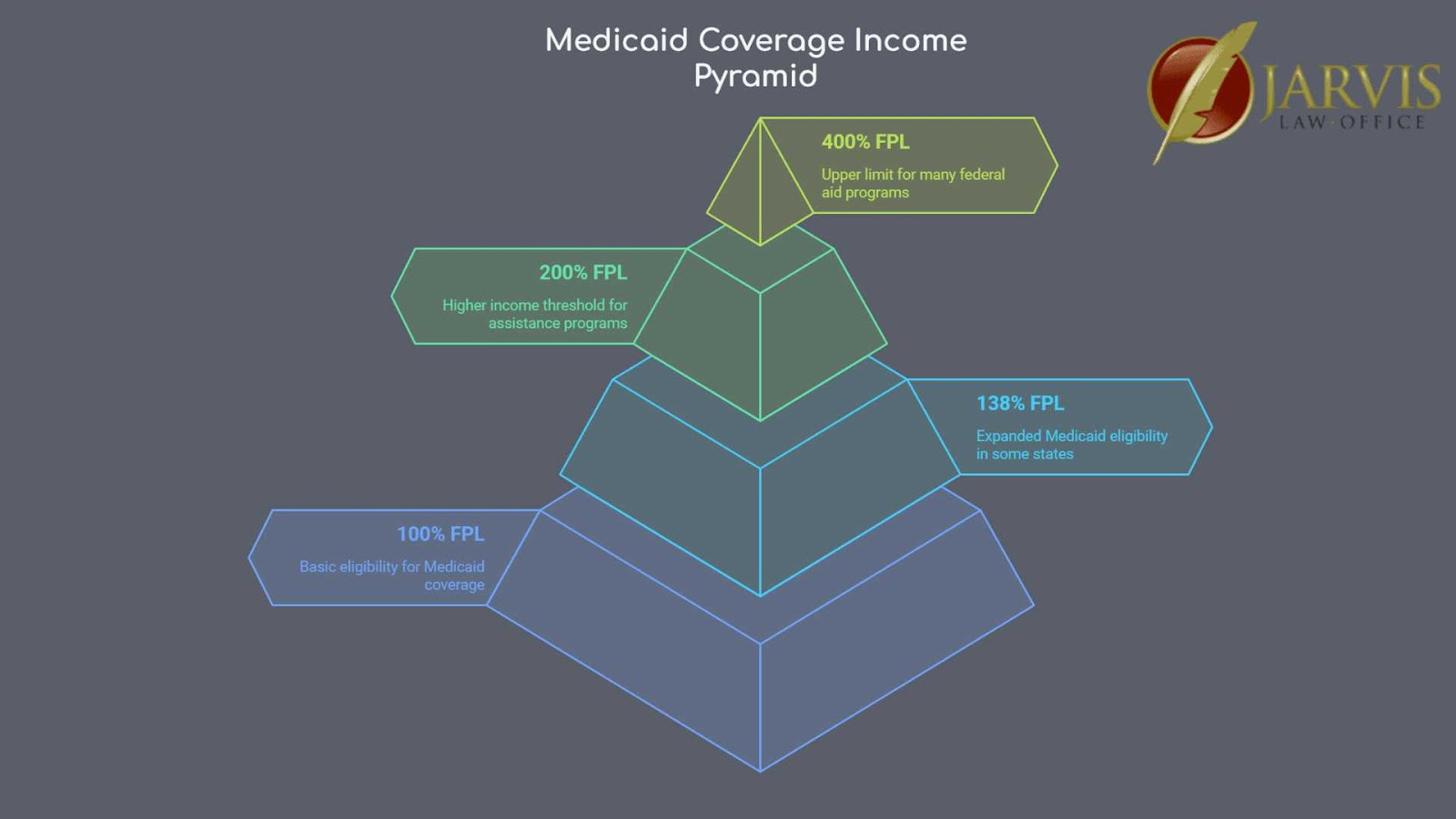

- The Federal Poverty Level (FPL) sets income limits for Medicaid eligibility and other assistance programs, with thresholds varying by household size and state.

- Medicaid expansion states cover adults earning up to 138% of the FPL, while non-expansion states have stricter income limits.

- ACA Marketplace subsidies help individuals earning between 100% and 400% of the FPL lower their health insurance costs.

- Strategic estate planning, including asset protection through trusts, can help individuals qualify for Medicaid while avoiding probate and unnecessary expenses.

What Is the Federal Poverty Level (FPL)?

The Federal Poverty Level (FPL) is an income measure set by the U.S. Department of Health and Human Services (HHS), andhelps to determine eligibility for Medicaid, ACA subsidies, SNAP (food assistance), and other government programs. Households with incomes below certain FPL percentages may qualify for financial aid or reduced-cost services.

How the Federal Poverty Level Works

FPL is adjusted annually to reflect inflation and cost-of-living changes. The income thresholds vary based on household size and location, with separate figures for Alaska and Hawaii due to their higher living costs.

Programs use different percentages of the FPL to define eligibility:

- Medicaid: In states where Medicaid has been expanded, adults qualify if their income is 138% of the FPL or lower. This includes a 5% income disregard, which is a portion of an applicant’s income that is excluded when determining eligibility, allowing more people to qualify for benefits.

- ACA Marketplace Subsidies: Households earning 100% to 400% of the FPL can receive premium tax credits to reduce health insurance costs.

- CHIP (Children’s Health Insurance Program): Income limits vary by state but often extend to 200% or more of the FPL.

- SNAP (Food Assistance): Most households must earn below 130% of the FPL to qualify.

2025 Federal Poverty Guidelines

The 2025 Federal Poverty Level (FPL) guidelines determine program eligibility until the next annual update. Below are the income thresholds for the 48 contiguous states and Washington, D.C.

Households larger than eight people should add extra income thresholds based on state-specific adjustments.

Knowing where your income falls on these scales is the first step in determining whether you qualify for Medicaid, ACA tax credits, or other assistance programs. If you’re near the limit for a specific program, checking with state agencies or using our FPL calculator can help confirm eligibility.

Annual Income Limits (48 Contiguous States & D.C.)

| Household Size | 100% FPL | 133% FPL | 138% FPL | 150% FPL | 200% FPL | 300% FPL | 400% FPL |

| 1 person | $15,650 | $20,815 | $21,597 | $23,475 | $31,300 | $46,950 | $62,600 |

| 2 people | $21,150 | $28,130 | $29,187 | $31,725 | $42,300 | $63,450 | $84,600 |

| 3 people | $26,650 | $35,445 | $36,777 | $39,975 | $53,300 | $79,950 | $106,600 |

| 4 people | $32,150 | $42,760 | $44,367 | $48,225 | $64,300 | $96,450 | $128,600 |

| 5 people | $37,650 | $50,075 | $51,957 | $56,475 | $75,300 | $112,950 | $150,600 |

| 6 people | $43,150 | $57,390 | $59,547 | $64,725 | $86,300 | $129,450 | $172,600 |

| 7 people | $48,650 | $64,705 | $67,137 | $72,975 | $97,300 | $145,950 | $194,600 |

| 8 people | $54,150 | $72,020 | $74,727 | $81,225 | $108,300 | $162,450 | $216,600 |

| Each additional person | +$5,500 | +$7,315 | +$7,590 | +$8,250 | +$11,000 | +$16,500 | +$22,000 |

Monthly Income Limits (48 Contiguous States & D.C.)

| Household Size | 100% FPL | 133% FPL | 138% FPL | 150% FPL | 200% FPL | 300% FPL | 400% FPL |

| 1 person | $1,304 | $1,735 | $1,800 | $1,956 | $2,608 | $3,912 | $5,217 |

| 2 people | $1,762 | $2,344 | $2,432 | $2,644 | $3,525 | $5,288 | $7,050 |

| 3 people | $2,221 | $2,954 | $3,065 | $3,331 | $4,442 | $6,663 | $8,883 |

| 4 people | $2,679 | $3,563 | $3,697 | $4,019 | $5,358 | $8,038 | $10,717 |

| 5 people | $3,138 | $4,173 | $4,330 | $4,706 | $6,275 | $9,413 | $12,550 |

| 6 people | $3,596 | $4,782 | $4,962 | $5,394 | $7,192 | $10,788 | $14,383 |

| 7 people | $4,054 | $5,392 | $5,595 | $6,081 | $8,108 | $12,163 | $16,217 |

| 8 people | $4,513 | $6,002 | $6,227 | $6,769 | $9,025 | $13,538 | $18,050 |

| Each additional person | +$458 | +$610 | +$633 | +$688 | +$917 | +$1,375 | +$1,833 |

Annual Income Limits for Alaska

| Household Size | 100% FPL | 200% FPL | 300% FPL | 400% FPL |

| 1 person | $19,550 | $39,100 | $58,650 | $78,200 |

| 2 people | $26,430 | $52,860 | $79,290 | $105,720 |

| 3 people | $33,310 | $66,620 | $99,930 | $133,240 |

| 4 people | $40,190 | $80,380 | $120,570 | $160,760 |

Annual Income Limits for Hawaii

| Household Size | 100% FPL | 200% FPL | 300% FPL | 400% FPL |

| 1 person | $17,990 | $35,980 | $53,970 | $71,960 |

| 2 people | $24,320 | $48,640 | $72,960 | $97,280 |

| 3 people | $30,650 | $61,300 | $91,950 | $122,600 |

| 4 people | $36,980 | $73,960 | $110,940 | $147,920 |

Medicaid Eligibility & Federal Poverty Guidelines

Medicaid provides free or low-cost health coverage for low-income individuals, families, and specific groups like pregnant women, children, and the elderly. Eligibility is based on income and household size, with limits set as a percentage of the Federal Poverty Level (FPL).

How FPL Determines Medicaid Qualification

To qualify for Medicaid, your household income must fall below a certain FPL percentage, which varies by state. Medicaid expansion under the Affordable Care Act (ACA) set the eligibility threshold at 138% of the FPL for most adults in participating states.

Medicaid eligibility rules differ in non-expansion states, where adults without children typically do not qualify unless they meet strict disability or caregiving criteria.

Key Medicaid Eligibility Thresholds by Group

| Eligibility Group | Typical FPL Limit |

| Adults (Expansion States) | 138% of FPL |

| Pregnant Women | 138% – 200% of FPL (varies by state) |

| Children (CHIP & Medicaid) | Up to 300% of FPL (varies by state) |

| Elderly & Disabled (SSI Recipients) | ~75% of FPL |

Medicaid Income Limits by State (2024-2025)

Each state sets its own income thresholds for Medicaid eligibility. The table below shows annual income limits for a family of four in select states.

In expansion states, nearly all adults earning up to 138% of the FPL qualify. In non-expansion states, Medicaid is usually only available to low-income parents, seniors, or disabled individuals.

| State | Medicaid Income Limit (138% FPL, Family of 4) | Expansion Status |

| California | $76,378 | Expanded ✅ |

| Texas | $41,400 | Not Expanded ❌ |

| New York | $76,378 | Expanded ✅ |

| Florida | $41,400 | Not Expanded ❌ |

| Ohio | $76,378 | Expanded ✅ |

Medicaid Expansion vs. Non-Expansion States

Not all states expanded Medicaid under the ACA. In non-expansion states, many low-income adults fall into the “coverage gap”, earning too much for Medicaid but too little for ACA subsidies.

Key Differences:

- Expansion States: Covers adults up to 138% of FPL with federal funding assistance.

- Non-Expansion States: Limits Medicaid to low-income families, disabled individuals, and seniors, often capping income limits well below the FPL.

To check your state’s Medicaid rules, visit HealthCare.gov or your state’s Medicaid website. If you don’t qualify for Medicaid, ACA subsidies might be an alternative.

ACA Health Insurance Subsidies and Federal Poverty Guidelines

The Affordable Care Act (ACA) provides subsidized health insurance for individuals and families who earn too much for Medicaid but still need financial assistance. These subsidies, also called premium tax credits—help lower the cost of monthly premiums for health plans purchased through the Health Insurance Marketplace.

How FPL Affects ACA Marketplace Plans

To qualify for ACA subsidies, your household income must be between 100% and 400% of the Federal Poverty Level (FPL). In some states, eligibility starts at 138% of FPL because Medicaid covers those below that level.

- 100% – 150% of FPL → Highest subsidies, low-cost or free “silver” plans with Cost-Sharing Reductions (CSR)

- 150% – 250% of FPL → Moderate subsidies, lower deductibles and copays available with CSR

- 250% – 400% of FPL → Lower subsidies, but premium tax credits still reduce costs

- Above 400% of FPL → Some may still qualify for subsidies under the American Rescue Plan & Inflation Reduction Act (extended through 2025)

2025 Income Thresholds for ACA Subsidies

| Household Size | 100% FPL | 400% FPL (Max Subsidy Eligibility) |

| 1 person | $15,650 | $62,600 |

| 2 people | $21,150 | $84,600 |

| 3 people | $26,650 | $106,600 |

| 4 people | $32,150 | $128,600 |

| 5 people | $37,650 | $150,600 |

| 6 people | $43,150 | $172,600 |

Medicaid vs. ACA Coverage: What’s the Difference?

Both Medicaid and ACA plans help with healthcare costs, but they serve different groups:

| Feature | Medicaid | ACA Marketplace Plans |

| Eligibility | Low-income individuals (≤138% FPL in expansion states) | 100% – 400% of FPL |

| Cost | Free or very low-cost | Subsidized, but may have deductibles & copays |

| Coverage | Comprehensive, including doctor visits, hospital stays, and prescriptions | Varies by plan, but covers essential health benefits |

| State Control | Administered by individual states | Federal program with state-run marketplaces |

If your income increases above Medicaid limits, you may transition to an ACA Marketplace plan with premium subsidies. Likewise, if your income drops, you might become eligible for Medicaid instead.

For the best coverage option, it’s important to check your FPL percentage and compare Medicaid vs. ACA eligibility.

Other Assistance Programs Tied to the Federal Poverty Level

Beyond Medicaid and ACA subsidies, the Federal Poverty Level (FPL) is used to determine eligibility for food assistance, children’s healthcare programs, and housing aid. Many federal and state programs rely on FPL percentages to make sure low-income individuals and families receive financial support.

Supplemental Nutrition Assistance Program (SNAP) Eligibility

The Supplemental Nutrition Assistance Program (SNAP), formerly known as food stamps, helps low-income households buy groceries. Eligibility is based on gross income (before taxes) and net income (after deductions), with limits set at 130% of the FPL in most states.

| Household Size | 130% of FPL (Annual Gross Income Limit) |

| 1 person | $20,345 |

| 2 people | $27,495 |

| 3 people | $34,645 |

| 4 people | $41,795 |

| 5 people | $48,945 |

| 6 people | $56,095 |

Some states expand SNAP eligibility to 200% of FPL, particularly for elderly and disabled individuals. Benefits are calculated based on income, expenses, and household size.

Children’s Health Insurance Program (CHIP) & FPL Limits

The Children’s Health Insurance Program (CHIP) provides low-cost or free healthcare coverage to children in families that earn too much for Medicaid but still need assistance. Income limits vary by state but typically range from 200% to 300% of the FPL.

In most states, CHIP covers doctor visits, prescriptions, dental care, vision services, and hospital stays. Some families may pay small premiums or copays depending on income.

Housing & Energy Assistance Programs Based on FPL

Several federal programs use FPL percentages to determine eligibility for housing aid, energy assistance, and utility bill relief:

- Section 8 Housing Choice Voucher Program: Helps low-income families afford rent. Generally, applicants must earn below 50% of the Area Median Income, but FPL is sometimes used as an additional qualifier.

- Low Income Home Energy Assistance Program (LIHEAP): Assists with heating and cooling costs for households earning below 150% – 200% of FPL, depending on the state.

- Temporary Assistance for Needy Families (TANF): Provides cash assistance and job training to low-income families. Income limits vary by state but often fall below 200% of FPL.

How to Calculate Your Federal Poverty Level (FPL) & Check Eligibility

Calculating your FPL percentage helps you see which benefits you might qualify for and what cost savings you can expect.

- Find Your Household Size

- Count all people living in your home who are included on your tax return.

- Do not include roommates or others who file taxes separately.

- Determine Your Annual Household Income

- Use your total gross income before taxes from all sources, including:

- Wages, salaries, and self-employment earnings

- Social Security benefits (excluding SSI)

- Unemployment benefits

- Alimony and rental income (if applicable)

- Use your total gross income before taxes from all sources, including:

- Compare Your Income to the FPL Chart

- Locate your household size on the latest FPL table.

- Divide your household income by the 100% FPL amount for your household size.

- Multiply by 100 to get your FPL percentage.

Example Calculation:

- A family of four with an annual household income of $48,000

- The 100% FPL level for four people is $32,150

- $48,000 ÷ $32,150 = 1.49 (or 149% of FPL)

This means the household earns 149% of the FPL, qualifying them for ACA subsidies but not Medicaid in expansion states, which typically require 138% of FPL or lower.

Protect Your Assets & Secure Your Future

Medicaid eligibility and asset protection don’t have to be complicated. With the right strategy, you can qualify for benefits, avoid probate, and keep control of your estate, without unnecessary costs or stress.

At Jarvis Law Office, we focus on trust-based planning and strategic asset management, making sure your wealth is protected while working alongside your existing financial advisor.

Ready to take the next step? Contact our team today to explore cost-effective estate planning solutions that fit your needs.